Your healthcare organization should consider several factors when deciding which patient financing programs to offer.

Some common problems providers look to solve with patient financing solutions include:

Increasing patient payments and decreasing the number of accounts that get sent to collections.

Strengthening the balance sheet through cash acceleration, so funds aren't tied up in long-term payment plans.

Reducing the burden on internal or 3rd-party staff, by removing the need to manage in-house payment plans.

Increasing patient satisfaction by making medical care more affordable.

Complete an inventory of your KPIs, capabilities, and resources.

What terms do you currently offer? Do the offered terms cover most of your patients' needs?

What percentage of your annual patient payments are from payment plans? What is your total outstanding payment plan balance?

What are your loss rates on in-house plans? Have you computed the full cost of managing the program beyond this one metric?

What is your current staffing burden? What resources are tasked with plan management activities, that could be redeployed to higher-value initiatives?

Do you have a patient experience platform in place that patient financing options need to integrate with?

If you're working with a patient financing vendor, what is the adoption of vendor plans relative to your total patient payments, and how much time does your team spend managing the program and reconciling balances?

These factors may point you toward in-house payment plans, recourse financing, non-recourse financing, patient affordability platforms, or a combination.

Social determinants of health (SDoH) can significantly impact a patient’s ability to afford medical care. At the same time, medical debt can affect SDoHs. Consider these questions:

What are the socioeconomic conditions among your patient base?

What’s the payer mix among your patient base? To what extent does your patient population have to pay out of pocket for care?

Can your patients afford the higher monthly payments that come with short-term plans, or do they need longer-term plans?

If you're working with a patient financing vendor, can payment plans involve interest or fees for patients? Do those programs promote equal affordability across your patient population?

For a non-recourse program what is the historical/likely approval rate, and for a recourse program what is the expected recourse rate?

How will each patient financing option influence your patients’ SDoHs?

Sharing the answers to these questing with any patient financing vendors you are considering will help them provide a specific proposal and ROI, and will give you a better sense of which options will be the right fit for you.

Finally, consider the total cost / benefit of patient financing programs to make an informed decision. Ask the vendors you are considering to share an ROI analysis and hold them accountable to the promised results. Here are some factors to look at when reviewing your options.

How does adding patient financing impact your collection rates? Providers typically collect 20-30% of patients' share of the cost of medical care after insurance.

How does the offered rate compare to your in-house plan economics? Industry-wide, the collection rate for in-house payment plans is about 70%.

When adding in your cost of capital, internal staff costs, and payments to early-out vendors and payment processors, the net to the provider is typically 50-60% of enrolled balances.

What are your economics after an account gets placed with bad debt? Bad debt liquidation rates are between 5-10% and the collection agency applies a contingency fee of 20-30% of what is collected.

Each type of patient finance vendor applies a different pricing model, and some vendors apply proprietary definitions to otherwise industry-standard terminology. It is therefore important to understand the differences and account for each component to accurately compare pricing across solutions.

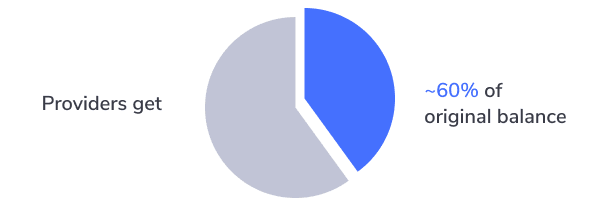

Recourse lenders advance capital to providers after deducting a financing charge of typically 15-20%. That means providers get paid 80-85% of the amount due after the patient enrolls and makes the first payment. But the realized pricing is much different for providers.

If a patient stops making payments, the balance is returned to the provider (typically after 3 missed payments). Recourse rates are about 20-30%, generally comparable to loss rates on in-house plans.

Most recourse finance providers charge ancillary fees as well; for example, a fee for onboarding and/or servicing accounts in addition to the finance charge.

The total cost to providers is typically 35-40% for finance charges, recourse rates, ancillary fees, and overhead for managing and reconciling returned accounts. That means providers typically end up receiving around 60% of the original patient balance.

Some recourse vendors also charge patients interest and fees on their accounts.

Low recourse rate quotes can be deceiving. Recourse vendors may publish “headline” rates much lower than the industry average. This may be accomplished through stricter eligibility criteria or by a hybrid recourse/non-recourse program with higher discount rates. Make sure you understand how your recourse rate is defined and how it affects overall program pricing.

Non-recourse lenders have lower rates to the provider, usually no more than 30%. These vendors generally cover a large part of their economics through interest and fees from the patient. Interest can be as high as 27%.

Enrollment is generally lower than other finance programs. Non-recourse lenders typically only approve ~50% of patients -- generally the most credit-worthy -- leaving the provider with the more economically stressed patients.

Because of this credit dynamic, a lower collection rate on the patient balances remaining with the provider typically offsets the higher yield from recourse plans.

With affordability platforms, the cost to providers is all-inclusive: a single discount rate that accounts for patient default risk, capital acceleration, platform, and end-to-end account servicing. There are no additional fees or interest to the provider or the patient.

The amount that providers are paid depends on the credit risk levels of patients and the repayment term of each plan. The total yield received by providers is typically 65 to 68%, with no recourse back to the provider.

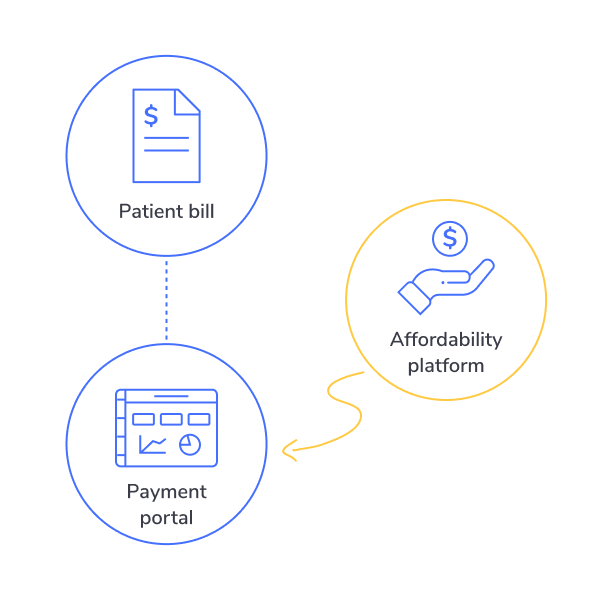

Affordability platforms are automated, so integrating them with existing patient workflows is easy. When a patient experience platform such as Flywire or EPIC MyChart is already deployed, affordability platforms provide an integrated payment plan experience, delivering even higher patient enrollment.

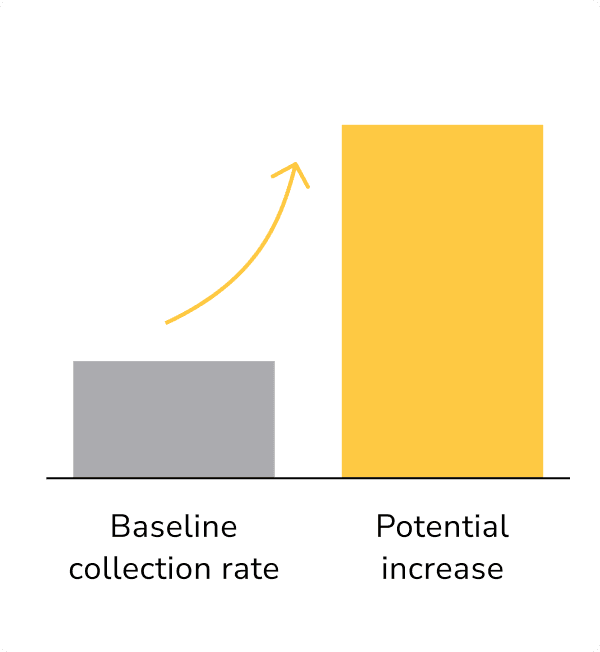

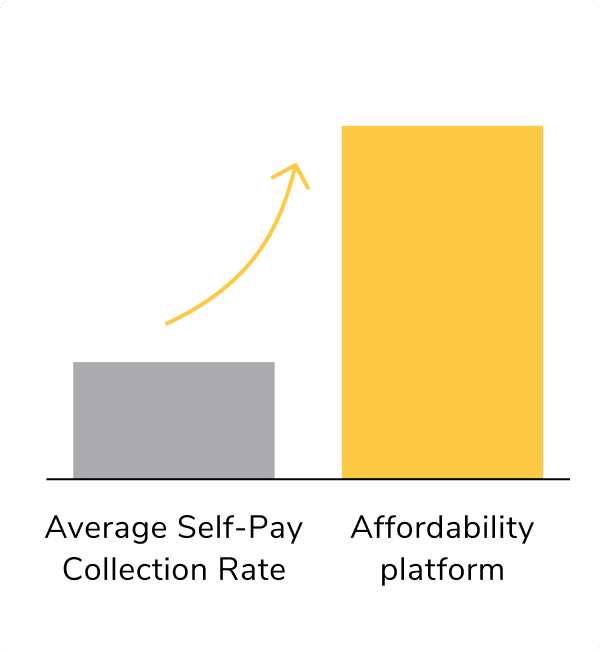

The result is that for all patient balances, whether through payment plans or lump-sum billing, overall collection rates typically increase by 20-30% with affordability platforms.

That means providers who normally collect 30 percent of unpaid patient bills would see their collection rate rise to between 36 and 39 percent - a significant increase without any new investment in staffing, technology, or additional workflows.

In-house plans

Traditional non-recourse vendors

Traditional recourse vendors

Affordability vendor: PayZen

Default rate

30%

N/A

Payment terms

0-24 months

0-48 months

0-60 months

Financing charge

5-30%

15%

Recourse percentages

No recourse

15-20%

Interest to patient

10-27%

0-18%

0%

Patient approval rate

100%

50%

Provider collection lift

Baseline

Often negative

0-10%

20-30%

Frees up resources, reduces bad debt expense and days in A/R

Constraints capital and internal resources

Selects for lowest risk patients only

Non-paying accounts returned; complexity and bad debt expense

Cash acceleration and provider resources unconstrained

Improves patient experience and affordability

Good for shorter plan length, limited extended terms

Interest, fees, and aggressive collection, limited patient adoption

Not real-time, relies on phone transfers by provider's team

Automated, real time enrollment, embedded in MyChart, Flywire, etc.

Early-out vendors and patient financing platforms play different, complementary roles in the revenue collection process. Early-out vendors are effective at securing payment from “good payers,” or patients who were already able to pay their bills within 30 days.

But what happens when patients need extended payment terms, and the provider wants cash acceleration? Patient financing solutions offer another way to improve yield and cash flow on patient balances.

There often can be tension between early-out vendors and patient finance vendors. If you are currently using an early-out vendor, it is important to align workflows and financial incentives.

A best practice is to carve out cash received from patient finance or affordability platforms, from the percentage the early-out vendor earns on collections. Many patient finance vendors are willing to share economics with the early-out directly for the promotion of the program.

It's also important to establish clear rules of engagement, including who engages patients when, and what is the longest repayment period an early-out may setup for provider in-house plans, so provider value from 3rd-party payment plans is maximized.

Emphasizing that all vendors need to work together in the best interest of the provider and patients, and providing clear direction to all parties on desired outcomes, is important for success.

The bottom line: Healthcare systems can benefit from using early-out vendors and patient financing platforms in tandem to maximize revenue capture. Make sure your vendors are working in your best interest, which may include economic arrangements between vendors that fit the needs of everyone involved.

Proactively offering longer payment terms to qualified patients, and making it easier for them to enroll, can increase collections rates by 20% to 30%.