Healthcare organizations have several options for patient financing—each with its own pluses and minuses. Here are the most common types, how they work, and what they can do for health systems and their patients.

In-house payment plans

Patient engagement portals

Recourse patient financing

Non-recourse patient financing

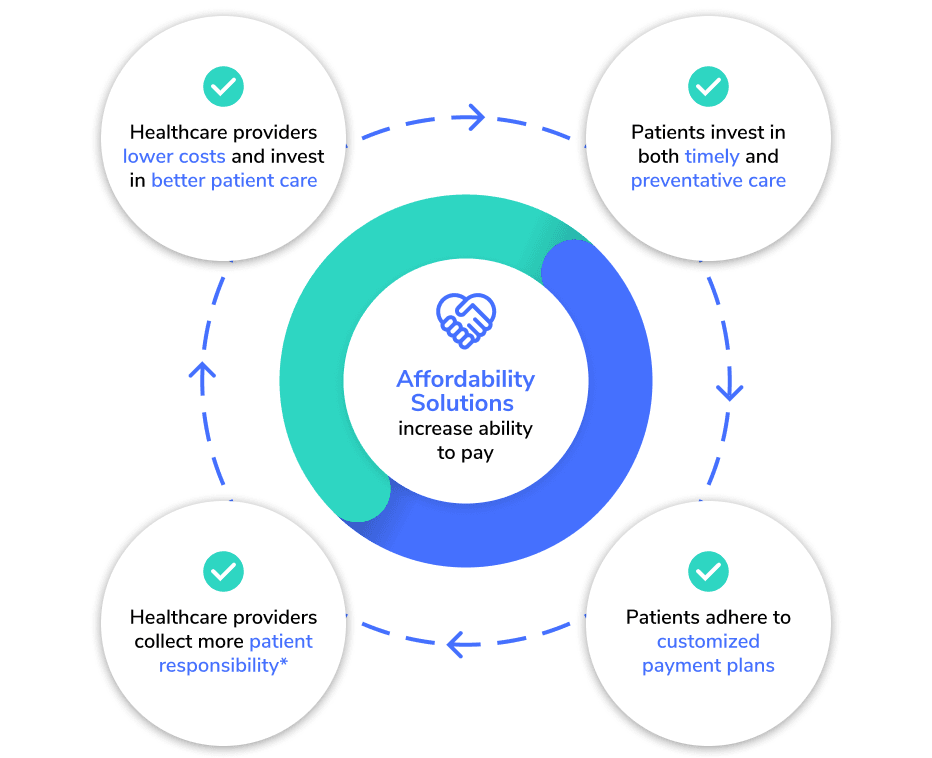

Affordability platforms

Many health systems operate in-house payment plans, essentially acting as a “bank” for patients by financing cost of care with their own operating capital.

Typically 100% of patients are eligible for in-house plans.

Terms and monthly payments are typically limited to 12 or 24 months.

Plans are often not proactively or consistently offered due to resource and technology constraints.

Often no patient self-enrollment or automatic payment capabilities.

The default rate for 12-month plans averages 30%.

In-house payment plans come with steep hidden costs beyond default rates, including internal cost of capital and the administrative burden on staffing, training, patient communication, and more.

With in-house payment plans, organizations either employ staff or engage an “early-out” call center vendor to handle incoming patient calls. Early-out vendors deal with patients during the first phase of the collection process to make sure they understand their bills and are trying to pay them.

Being the bank means….

Long cash cycles that adversely affect operating flexibility and financial strength.

Overall collection rates affected by payment plan enrollment and adherence efforts.

Exposure to inflation risk and uncertain repayment in challenging economic times.

Time-value of money erodes the value of payment plan collections.

Being the “bad guy” when collecting on patient plans, impairing patient experience, trust, and brand perception.

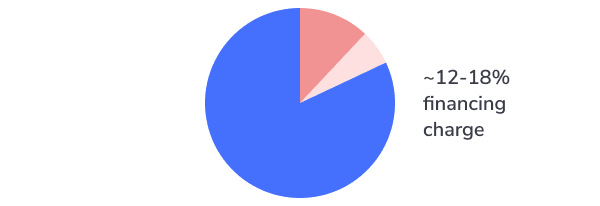

As an alternative or complement to in-house collections, healthcare systems can engage a third-party patient financing company such as a recourse vendor.

The vendor pays the hospital or health system for the care rendered minus a financing charge, typically 12-18%.

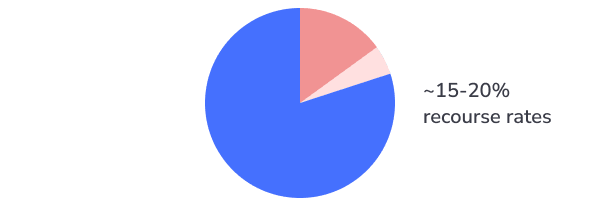

A “recourse rate” also applies, and is typically 15-20%.

The vendor accepts 100% of patients for a payment plan, often with different program terms depending on the patient's ability to pay.

Patients may be charged interest and fees. 0% interest options can lead to interest rates as high as 18% or more, retroactively applied to outstanding balances.

Recourse plans can be for a term of up to 60 months. Some vendors will extend terms even further.

While most patients pay their loans, historically 15% to 20% of recourse accounts are returned to the provider. When that happens, the lender returns the past-due debt to the hospital or health system and pulls back the money it previously paid. It’s then up to providers to collect those unpaid debts.

When healthcare providers choose to work with recourse lenders, they risk the chance that they’ll need to reassume the medical debt and collect it themselves.

This leads to additional cost and complexity in the revenue cycle, which must be considered when evaluating recourse programs:

Providers will need to allocate resources to manage patient accounts that are returned by the vendor.

Finance teams have additional workflows to reconcile account balances and hold escrow reserves against future recourse returns.

With non-recourse programs, the vendor retains the account even if the patient doesn’t pay. Providers keep the money they receive from the vendor and don’t have to be concerned with managing unpaid debt. It’s up to the lending company to collect the remaining payments from patients.

The vendor pays the provider a discounted right up-front and assumes the repayment risk on patient balances.

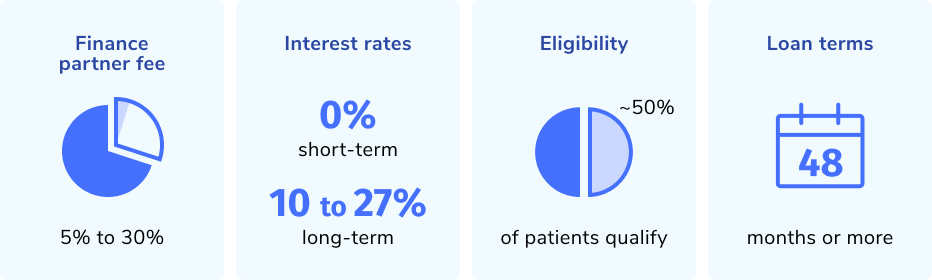

Non-recourse finance partners typically charge the provider a 5% to 30% fee, depending on the interest rate it charges patients and the loan term.

Most loans are for terms of 48 months or less.

Interest rates are often 0% for short-term loans or promotional periods, then increase to between 10% and 27%. Promotional periods are usually between 12 and 24 months long.

Patients must complete a credit application to be eligible for a payment plan. Typically, only ~50% of patients qualify.

With non-recourse financing, providers may receive between 70% and 95% of the balances for enrolled patients. But non-recourse finance partners usually approve only about 50% of patients, so the net impact on collection rates is often modest and can even be negative.

That’s because non-recourse lenders take the highest credit-quality, lowest-risk patients and leave higher-risk patients for the provider’s in-house payment plans, where non-performing accounts often offset any lift from the finance program.

Traditional recourse and non-recourse patient financing options can help accelerate cash flow and improve a provider’s balance sheet, but they often only marginally increase the number of paying patients.

Both types of financing can be difficult to administer, and call centers often provide a poor patient experience that can harm patient satisfaction.

Additionally, recourse reconciliation can be a complex process for provider organizations and can dampen any benefits the organization may have received.

Increasingly, health systems are deploying patient engagement portals from companies such as Flywire and Cedar, or the MyChart patient portal from dominant EHR system vendor EPIC.

These portals enable automated and personalized patient communications and self-service capabilities to improve and digitize patient experiences. They can streamline complex Patient Financial Experience challenges such as billing, statement consolidation, and payment plan offerings.

But patient engagement portals were not designed to address the core issue of patient affordability. They tend to focus on bill contextualization and checkout, with limited payment options.

Patients can often self-enroll in a payment plan through these platforms, but enrollment may be limited to whatever payment options the provider already has in place.

Additional payment plans options may be data-driven, or they may be “one-size-fits-all.”

Plans typically have short repayment terms, limiting affordability for patients with higher balances.

Providers still carry these payment plans on their books, requiring the same staffing and servicing investments, long cash cycles, and repayment risk of traditional in-house plans.

Some patient engagement portals, Such as Flywire and EPIC MyChart, support integration with 3rd party patient financing solutions. Such platforms increase the options available for patients and offer greater financial flexibility for providers.

A relatively recent patient finance option is an affordability platform, such as PayZen, which combines the best features of recourse and non-recourse programs with a patient-centric approach, bringing a new payment plan model to healthcare.

Here’s a primer on this approach:

100% of patients can enroll, with no credit application or impact to their credit score.

The platforms provide immediate, 100% non-recourse cash acceleration on all plans.

Patients are never charged interest or fees.

Providers never risk reassuming patient accounts or returning the accelerated funds they receive.

Affordability platforms are fully automated, so they don’t impact providers’ staff.

They engage patients proactively across physical and digital channels to maximize patient adoption.

They use technology to provide the simple, intuitive patient experience expected by today's healthcare consumer.

They integrate easily with leading patient engagement and check-out platforms.

Go-lives typically take just a few weeks, with no IT investment needed.

Affordability platforms create personalized payment plan options based on each patient's unique ability to pay.

Personalization is a primary differentiator for affordability platforms. With advancements in AI, providers can now make intelligent financing offers based on a patient’s specific financial circumstances.

Platforms such as PayZen instantly analyze thousands of attributes per patient to develop a custom payment plan.

Each payment plan is based on the patient’s ability to pay, which directly improves the rate of collections and maximizes provider cash flow.

Personalization also improves the patient experience by offering peace of mind that they can afford the care they need.

Reducing the risk that people will defer or forgo care out of financial concerns ultimately translates to healthier populations, which in turn lowers the cost of care.

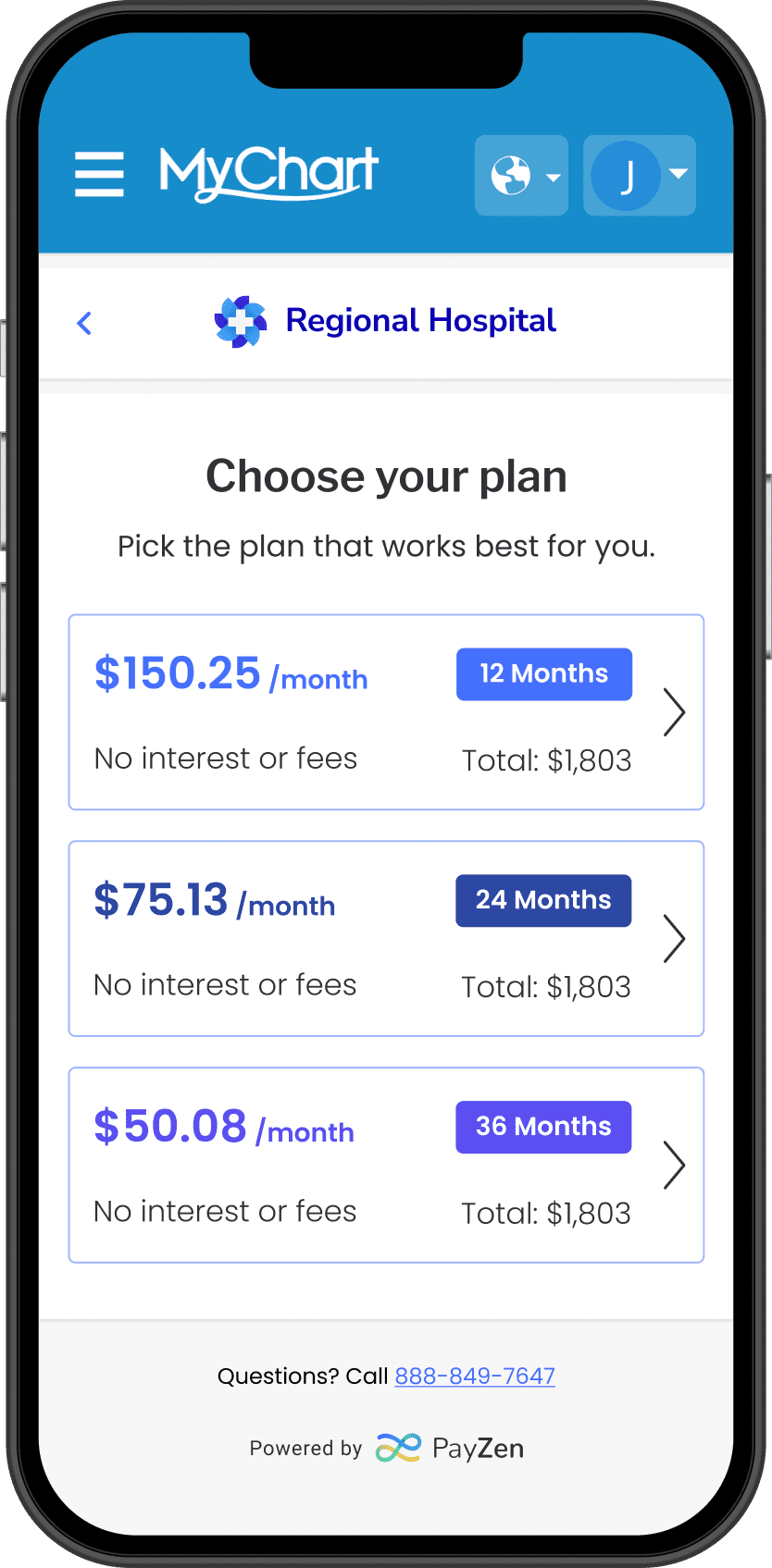

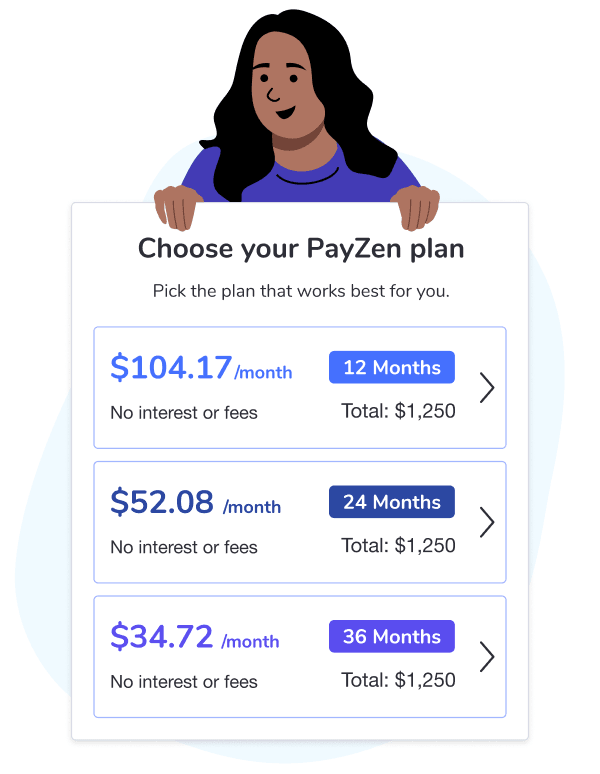

With affordability platforms, patients benefit from zero-interest repayment terms up to 60 months with no credit application. Patients can manage their plans online directly within existing patient-facing applications, maximizing ease of use and patient adherence.

By improving healthcare affordability, solutions such as PayZen also help solve the core issues affecting collection rates on payment balances.

Depending on your specific usage of payment plans, your organization may see cash acceleration benefits while:

Reducing the cost of collections

Avoiding the expense of managing in-house plans and many 3rd-party programs

Eliminating the risk of re-assuming patient accounts

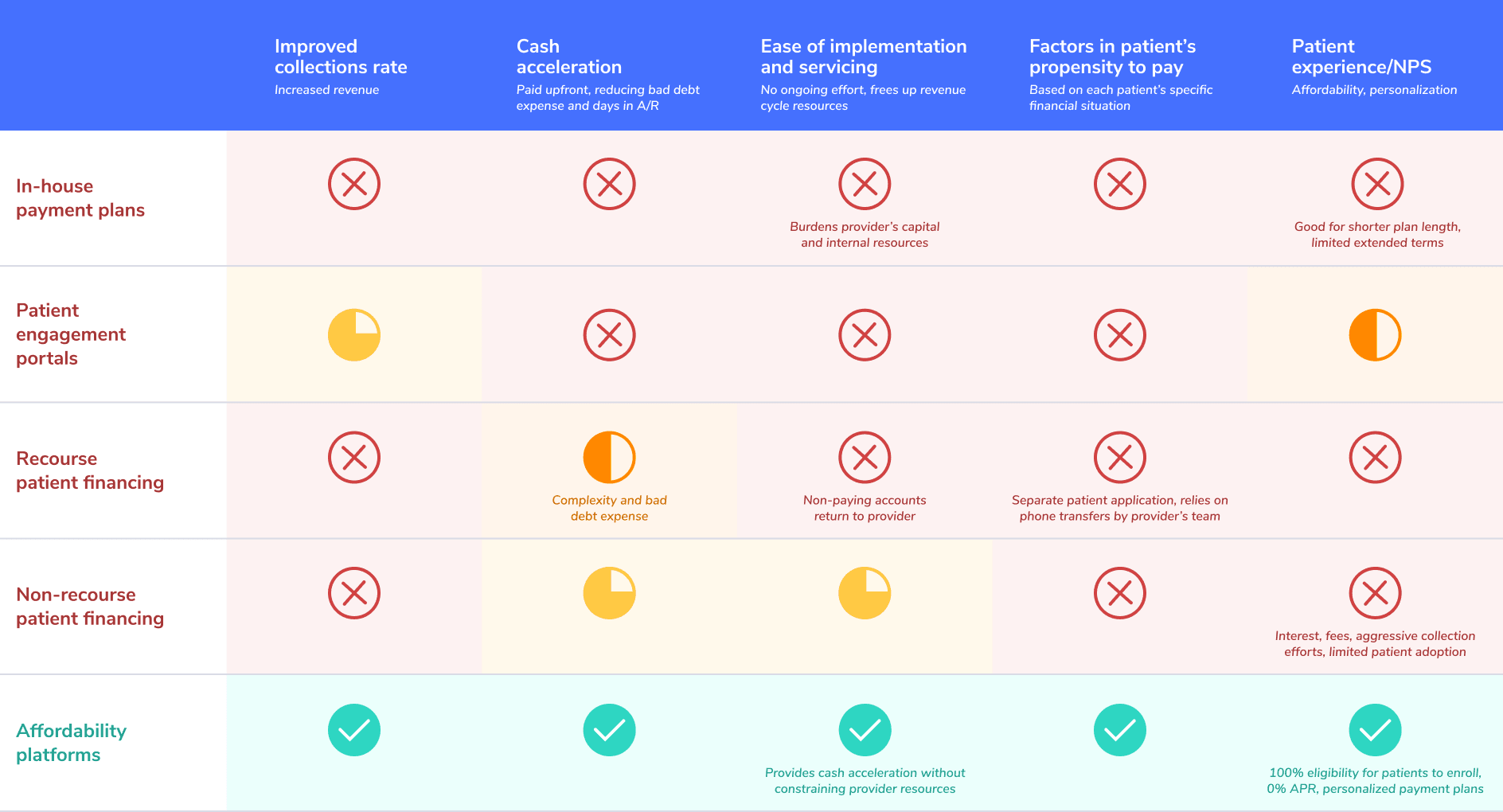

The chart on the next page summarizes key capabilities and benefits of the various patient financing solutions available to providers. 👉